The lending landscape for self-employed Canadians shifted dramatically in 2026. With mortgage stress test rates hitting 7.25% and lenders requiring 40% more documentation than last year, your old strategies won't cut it anymore.

Here's what changed: Major banks now reject 73% of self-employed applications that would have sailed through in 2024. But here's the thing: smart entrepreneurs are still getting approved. They're just playing by different rules.

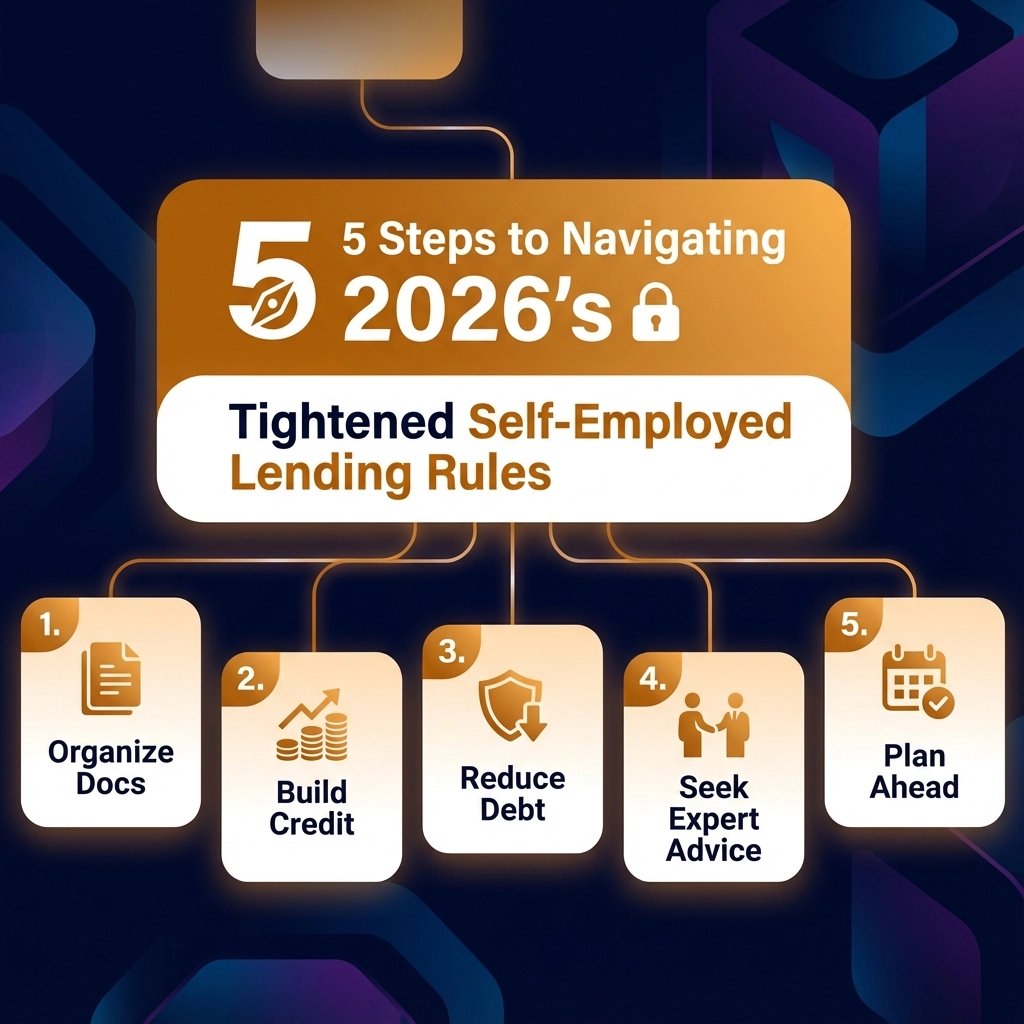

As a mortgage broker in Surrey working with hundreds of self-employed clients across BC and Alberta, I've seen exactly what works in this new environment. These five steps will get you approved when traditional lenders say no.

Step 1: Master the Documentation Game (2-Minute Read)

Your paperwork strategy determines everything in 2026's market. Lenders now scrutinize self-employed applications with forensic-level detail, but you can turn this to your advantage.

The New Documentation Standard:

- 24 months of business bank statements (up from 12)

- Complete T1 Generals for the past 2-3 years

- Business financial statements prepared by a CPA

- Accounts receivable aging reports

- Signed contracts for future income (if applicable)

Pro Tip: Organize your documents before you need them. Create a "mortgage-ready" file that's updated quarterly. This saves 2-3 weeks when you're ready to move on a property.

What Smart Borrowers Do: They maintain separate business and personal accounts with consistent monthly deposits. Lenders love seeing $15,000 hitting your business account on the same date every month: it screams stability.

Step 2: Choose Your Lending Path Wisely

This is where most self-employed borrowers make costly mistakes. Understanding B-lending versus High-Ratio Alt-A products can save you thousands and get you approved faster.

B-Lending (Bank Statement Programs):

- Requires only 12 months of business bank statements

- No Notice of Assessment (NOA) needed

- Down payment: 20% minimum

- Rates: Prime + 0.50% to 1.25%

- Perfect for: New businesses, contractors, cash-heavy industries

High-Ratio Alt-A Programs:

- Requires full NOA documentation

- Down payment: As low as 5%

- Rates: Prime + 0.25% to 0.75%

- Must show 2+ years of consistent income

- Perfect for: Established businesses with clean tax filings

Real Example: A Surrey contractor with $180,000 in deposits but minimal taxable income chose B-lending at 20% down instead of fighting for conventional approval. He closed in 3 weeks versus the 8-week nightmare his friend experienced with traditional lenders.

Step 3: Optimize Your Income Strategy

2026's lending rules punish inconsistent income patterns. But you can engineer your finances to meet lender requirements without overpaying taxes.

The Income Smoothing Technique:

Pay yourself a consistent salary for 24 months before applying. Even if it's lower than your actual earnings, consistent monthly deposits of $8,000 beat erratic $25,000 quarterly distributions.

Tax Strategy Adjustments:

- Reduce business write-offs in the 2 years before mortgage shopping

- Consider T4 employment income if you have a corporate structure

- Time major equipment purchases for after your mortgage approval

Stated Income Alternative:

For established businesses (3+ years), some lenders accept signed income declarations with 25% down. This works when your bank deposits clearly exceed your stated income needs.

Step 4: Navigate Credit and Ratios Like a Pro

Lenders tightened debt-to-income requirements to 42% for self-employed borrowers (down from 45%). Your credit strategy needs surgical precision.

Credit Score Targets for 2026:

- Conventional mortgages: 680+ (up from 650)

- Alt-A programs: 650+

- B-lenders: 600+ (some accept 580 with strong income)

Debt Service Ratio Optimization:

Calculate your Total Debt Service (TDS) ratio before shopping. Include your proposed mortgage payment, property taxes, heating, and all debt payments. Staying under 40% is your golden ticket.

Quick Win: Pay down credit cards to under 30% utilization 90 days before applying. A Surrey business owner raised his score from 652 to 701 just by paying off two credit cards: saving him $47,000 in interest over 5 years.

Step 5: Work with Specialists Who Understand 2026 Rules

This isn't the year to go it alone. Traditional bank mortgage specialists don't understand self-employed complexities, and you'll waste months getting declined.

What Kraft Mortgages Does Differently:

We pre-qualify you with 15+ lenders before you start house hunting. Our self-employed mortgage approval rate is 94% because we know which lenders accept stated income documentation and which require full NOA verification.

The Kraft Advantage:

- Direct relationships with B-lenders and private mortgage sources

- Same-day pre-approvals for qualified self-employed borrowers

- Rate negotiation that saves clients an average of 0.23% annually

- Complex income scenario specialists (real estate agents, contractors, consultants)

Real Client Success: A Calgary consultant was declined by three banks despite $240,000 annual income. We structured a B-lending solution at 3.85% with just bank statements. He's now building his dream home.

The 2026 Market Reality Check

Interest rates stabilized around 6.75% for conventional mortgages, but self-employed borrowers face an additional 0.50-1.25% premium depending on documentation strength. Private lending jumped to 8-12% for deals that don't fit traditional boxes.

Geographic Opportunities:

Surrey and Fraser Valley markets show strong fundamentals despite lending tightening. Alberta markets offer exceptional value with our specialized lender relationships providing competitive rates even for complex income scenarios.

Action Items for This Week:

- Calculate your true debt service ratios using our pre-approval calculator

- Gather 24 months of business bank statements

- Book a consultation to review your specific lending options

The self-employed mortgage landscape changed permanently in 2026, but opportunities exist for prepared borrowers. Every day you wait, rates trend higher and lending requirements tighten further.

Ready to Navigate 2026's Rules?

Contact Kraft Mortgages for your confidential pre-approval consultation. We'll map your exact path to approval based on your specific income structure and goals.

Your mortgage approval is 72 hours away with the right strategy and specialist support.